All articles

Policy Breakdown Leaves ACA Enrollees Facing Steep, Sudden Premium Increases Nationwide

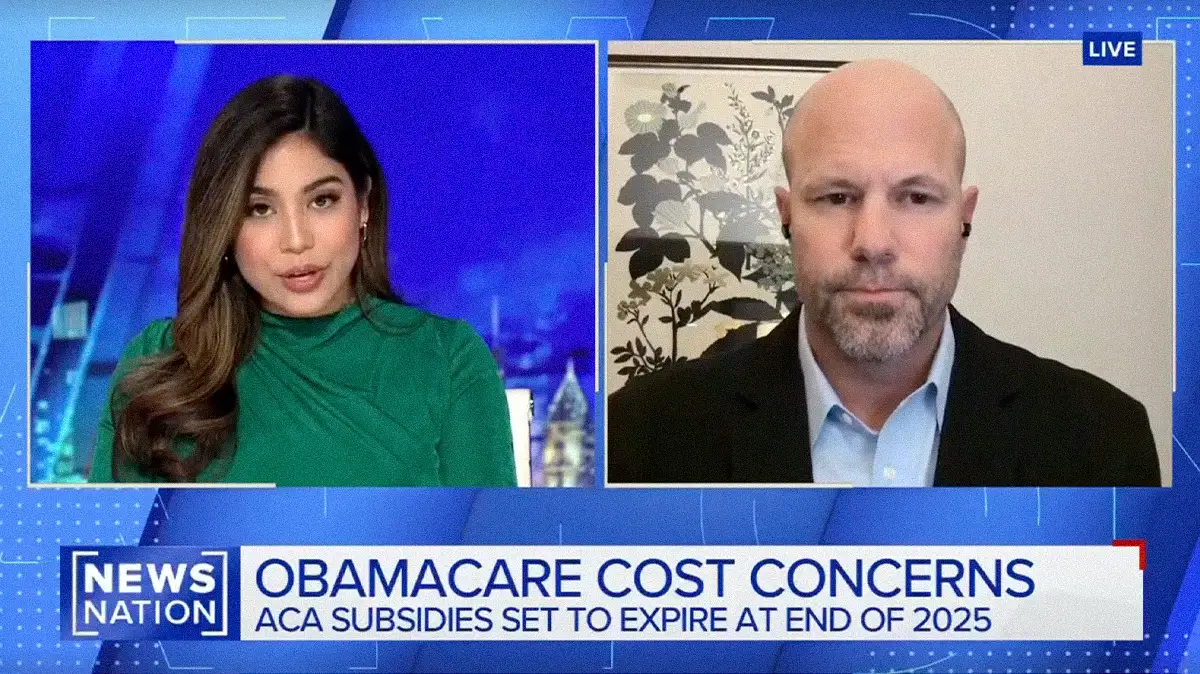

ACA subsidies expired at the end of 2025, leaving millions to face sudden premium shocks. Erik Wissig, COO and CFO at SureCo, links the cliff to policy failure and a system that pushes individuals to the margins.

Make Benefits Brief News one of your go-to sources on Google

Those folks have a complete fall-off of the subsidy they have been receiving over the past few years. And with that, you're going to see potentially a thousand dollars or more increase in their premium come a few days from now.

Erik Wissig

More than 20 million Americans have faced a sharp health insurance price hike as federal subsidies for Affordable Care Act plans expired at the end of 2025. Average premiums have risen 114%, with some families in states like Texas facing four-figure increases. A transition plan never came together before the end of the year, as Congress adjourned without a deal and left families to shoulder the impact.

Insight into the mechanics behind these price hikes comes from Erik Wissig, Chief Operating Officer and Chief Financial Officer at SureCo, who discussed the issue in a recent NewsNation interview. A Co-Founder of Hixme, Wissig helped pioneer the employer benefit model now known as ICHRA, shaping his perspective on the market’s structural weaknesses and potential paths forward.

The design of the ACA means that individuals and families earning just above 400% of the federal poverty line lost subsidies all at once, with no glide path to soften the blow. Wissig confirms the severity of this abrupt cut-off for this specific group. "Those folks had a complete fall-off of the subsidy they had been receiving over the past few years. And with that, you saw potentially a thousand dollars or more increase in their premium," says Wissig.

- Compromise, cancelled: The sudden price hike, he explains, is the direct result of a larger breakdown at the political level. "The ultimate failure is really a lack of ability for a compromise to come into place. The fact that we have not been able to find that plan before January, that's where the difficulty lies."

According to Wissig, the subsidy expiration acted as a catalyst, multiplying pressures already building beneath the surface of a system where Americans are often paying more for less. The political uncertainty around extending subsidies had led many insurers to price that risk into their plans months in advance. Providers, in turn, adjusted their own business models, layering their changes on top of baseline medical inflation.

- Cost cascade: The result is a compounding effect, as seen in states like North Carolina, where subsidy expirations are combining with state-approved rate hikes. "It's a combination of all of it. You have consistent 8% to 10% medical inflation, but on top of that, this year you have this uncertainty and the fall-off of the subsidies that have put the average increases up above 20%," notes Wissig. "For those people losing the subsidy, it just multiplies it."

- The one-two punch: According to Wissig, the dynamic reveals a fundamental flaw in the current approach: the subsidies are a temporary fix layered on top of an already expensive system. With some projections showing healthcare could consume 40% of a typical family's income within a decade, the model isn't a long-term solution. "To lower costs right now, you need that transition off of the subsidies. An extension of one to two years would enable policymakers to bring in more consumer-based programs, like expanding the HRA model. Allowing an HSA to support premium payments would also be fantastic to see."

That temporary extension, he says, would create the breathing room to implement a more durable solution. His proposed long-term fix involves leveraging the consumer-centric tools he helped pioneer. By transitioning employers to an individual-based model like ICHRA, he says, the system can attract a wider mix of people to the individual insurance market, a step that is key to stabilizing prices.

But for Wissig, these policy suggestions are simply tools to address a more fundamental design flaw. "The big failure here is that the individual, the person that is actually buying the insurance, is not really at the center of the decision. Until we have that system in place, we're going to see some very difficult and challenging years," he concludes.